January 31, 2020

PAO Severstal (MICEX-RTS: CHMF; LSE: SVST), one of the world’s leading steel

and steel-related mining companies, today announces its Q4 & FY2019

financial results for the period ended 31 December 2019.

CONSOLIDATED FINANCIAL RESULTS FOR THE FOURTH QUARTER ENDED 31

DECEMBER 2019

Notes:

- EBITDA represents profit from operations plus depreciation and

amortisation of productive assets (including the Group’s share in depreciation

and amortisation of associates and joint ventures) adjusted for gain/(loss) on

disposals of PPE and intangible assets and its share in associates’ and joint

ventures’ non-operating income/(expenses). A reconciliation of EBITDA to profit

from operations is presented in Severstal’s annual financial

statements. - Free Cash Flow (“FCF”) is determined as the aggregate amount of the

following items: Net cash from operating activities, CAPEX, proceeds from

disposal of PPE, interest received and dividends received. A reconciliation of

FCF to net cash from operating activities is presented in Severstal’s annual

financial statements. - Basic EPS is calculated as profit for the period divided by the

weighted average number of shares outstanding during the period: 825.4 million

shares for Q4 2019, 825.4 million shares for Q3 2019, 824.6 million shares for

2019, 817.1 million shares for 2018.

Q4 2019 vs. Q3 2019 ANALYSIS:

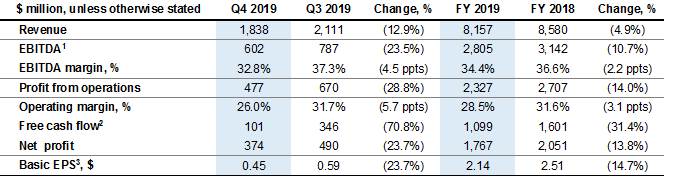

- Group revenue declined by 12.9% q/q to $1,838 million (Q3 2019: $2,111

million) due to lower steel sales volumes and adverse pricing dynamics for

steel and raw materials. - Group EBITDA declined by 23.5% q/q to $602 million (Q3 2019: $787 million),

reflecting topline decline partially offset by a reduction in cost of sales.

The Group’s vertically integrated business model delivered an EBITDA margin of

32.8%, maintaining its position as one of the highest in the industry

globally. - FCF totalled $101 million (Q3 2019: $346 million), primarily reflecting

lower earnings and higher CAPEX, offset by positive changes in net working

capital q/q. - Profit for the period totalled $374 million (Q3 2019: $490 million) and

includes a FX gain of $74 million. - Cash CAPEX amounted to $431 million (Q3 2019: $311 million).

- Net debt increased to $1,570 million at the end of Q4 2019 (Q3 2019: $1,300

million), primarily reflecting a reduction in cash balances as a result of the

dividend payment. - Severstal is committed to returning value to its shareholders whilst

managing and maintaining a comfortable level of debt. Severstal’s financial

position remains strong with a Net debt/EBITDA ratio of 0.6 as at the end of Q4

2019. The Board of Directors has therefore recommended a dividend of 26.26

roubles per share for Q4 2019.

FY2019 vs. FY2018 ANALYSIS:

- Group revenue declined by 4.9% y/y to $8,157 million (FY2018: $8,580

million). This drop in revenue y/y was a result of weaker pricing for steel

products. - Group EBITDA was 10.7% lower y/y at $2,805 million (FY2018: $3,142

million), primarily reflecting lower revenues offset by a reduction in cost of

sales. The Group’s EBITDA margin remained high at 34.4% (FY2018: 36.6%). - The Company generated $1,099 million of FCF, which represents a decline of

31.4% y/y (FY2018: $1,601 million), mainly reflecting a decline in EBITDA and

CAPEX growth y/y.

FINANCIAL POSITION HIGHLIGHTS:

- At the end of Q4 2019, cash and cash equivalents stood at $1,081 million

(Q3 2019: $1,317 million), reflecting dividend payout partially offset by FCF

generation. - Gross debt remained almost flat at $2,651 million (Q3 2019: $2,617

million). - Net debt increased to $1,570 million by the end of Q4 2019 (Q3 2019: $1,300

million), primarily reflecting a reduction in cash balances. The Net

debt/EBITDA ratio amounted to 0.6 at the end of Q4 2019 (Q3 2019: 0.4).

Severstal’s Net debt/EBITDA remains one of the lowest amongst steel companies

globally and enables the Company to maintain a comfortable level of debt,

whilst continuing to return value to its shareholders. - The Group’s liquidity position remains strong, with $1,081 million in cash

and cash equivalents in addition to unused committed credit lines and overdraft

facilities of $1,250 million, more than covering the short-term principal debt

of $282 million.

Alexander Shevelev, CEO of Severstal Management, commented:

“The fourth quarter of 2019 was challenging for steel producers globally,

with both steel demand and prices in decelerating and recovery only starting in

December 2019. In this environment, Severstal’s vertically integrated business

model, combined with the flexibility of our multiple distribution channels,

successfully supported our EBITDA margin, which was 33% in Q4 2019. We are

proud of our operational results for 2019 with 38% growth in coking coal and

14% growth in iron ore concentrate sales volumes.

Our overall safety performance improved in 2019 and our LTIFR decreased by

36% to 0.61 (2018: 0.95), which is 27% below our goal for the year of 0.84.

However, we deeply regret that during the year there were two fatalities among

our staff and three among our contractors.

On the environmental side the amount of atmospheric emission of pollutants

per tonne of steel products fell by 7% in the year. In Q4 2019, we set

ourselves a target to increase the share of own energy generation using

secondary sources to 95% by 2025, which is an example of minimising both costs

and our environmental impact.

I am pleased that our efforts to transform the company which we started in

2018 in line with our 5-year strategy continue brining fruits. In 2019, we

earned additionally $224 million at the EBITDA level and are remaining one of

the lowest costs steelmakers globally.

Positive momentum continues with our investments in new technologies. Our

division Severstal Ventures made three new investments recently which should

enable us to offer our customers new materials with unique properties in the

future.

The Board remains confident in its outlook and is recommending a dividend of

26.26 roubles per share for Q4 2019.”

DIVIDEND

The Board of Directors has recommended a dividend of 26.26 roubles per share

for Q4 2019. Approval of the dividend is expected to take place at the

Company’s AGM on 5 June 2020. The record date for participation in the AGM is

11 May 2020. The recommended record date for the dividend payment is 16 June

2020. Approval of the record date for the dividend payment is also expected to

take place at the Company’s AGM on 5 June 2020.

OUTLOOK

The Phase 1 agreement between China and the USA and progress with the Brexit

deal in Europe have reduced global economy risks and boosted market optimism

which should support steel demand in the long term. After the sharp drop in Q4

2019 global steel prices seem to be turning the corner in Q1 2020 thanks to

restocking and production cuts.

In Russia, the construction sector will again remain a key steel demand

driver in 2020, supported by the expected implementation of the National

projects. Good pricing in the Russian market is attributable to the

appreciation of the rouble and limited steel supply due to current

reconstruction works at some mills.

Despite a number of potential headwinds on both the export and domestic

markets, Severstal’s low cost position allows us to remain competitive in the

market. The Board remains confident in the resilience of the Company’s business

model relative to its local and global peers.

NOTES

- Full financial statements are available at

//www.severstal.com/eng/ir/results_and_reports/financial_results/index.phtml - The Annual Report 2019 will be available at

//www.severstal.com/eng/ir/results_and_reports/annual_reports/index.phtml

Leave a Reply